Saving money can feel like an impossible task, even when you’re earning a decent income. Despite your best intentions, certain habits and hidden pitfalls could be sabotaging your financial goals without you even realizing it. The good news is that by identifying these issues, you can start making changes to build a more secure financial future. Here are 12 shocking reasons you’re struggling to save money—and how to turn things around.

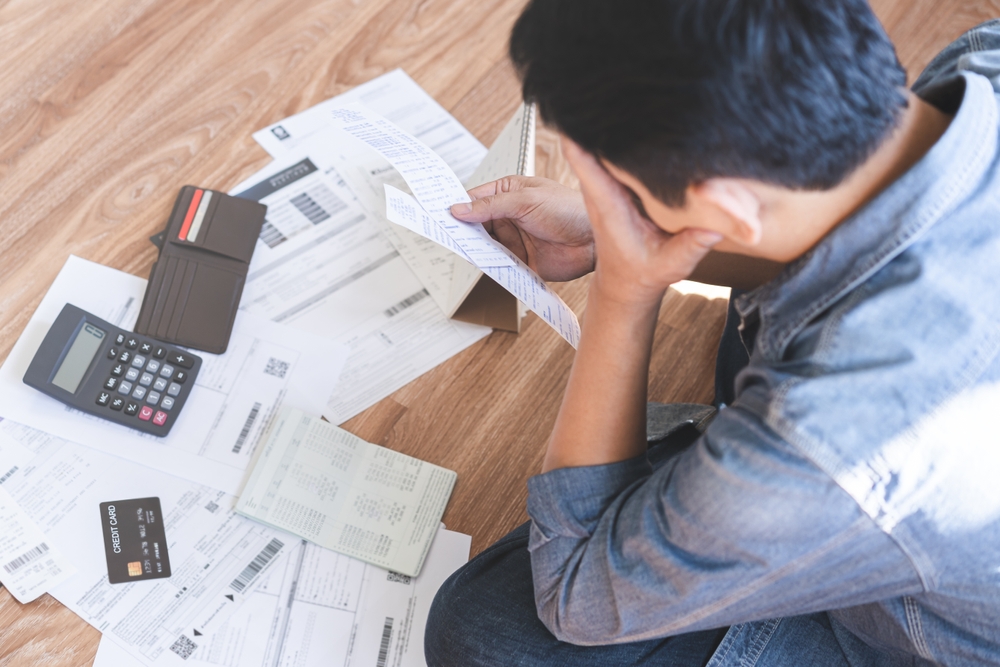

1. Credit Card Debt

According to NerdWallet, high-interest credit card debt can drain your finances and leave you trapped in a cycle of minimum payments. Carrying a balance month to month means you’re spending more on interest than paying down the principal. This reduces the amount of money you have available to save or invest. Credit cards can also encourage overspending since it’s easy to lose track of how much you owe. Pay off your balances as quickly as possible and stick to using credit only for essential expenses.

2. Impulse Purchases

Impulse buying is one of the biggest obstacles to saving money. Psychology Today reveals that whether it’s grabbing something at the checkout line or falling for online sales, these unplanned purchases can quickly add up. Retailers use tactics like discounts and limited-time offers to tempt you into spending more than you planned. Without realizing it, you might be prioritizing instant gratification over long-term financial goals. Combat this by waiting 24 hours before making non-essential purchases to determine if you truly need the item.

3. You’re Living Beyond Your Means

Research from Investopedia shows that keeping up with trends or trying to maintain a lifestyle that doesn’t match your income can wreak havoc on your finances. Whether it’s buying a luxury car, dining out frequently, or splurging on designer items, living beyond your means leaves little room for savings. Over time, this behavior often leads to debt, making it even harder to save. Instead of comparing yourself to others, focus on living within your budget and prioritizing your future. Building a lifestyle that fits your income is key to financial success.

4. You Don’t Have a Budget

Insights from The Balance reveal that without a clear budget, it’s impossible to track where your money is going, making it easy to overspend. Many people underestimate small expenses, which add up over time and drain potential savings. A budget serves as a financial roadmap, showing you exactly how much you can spend and save each month. If you’re not budgeting, you might be spending more than you earn, leaving nothing for savings. Start by tracking your income and expenses and allocating a portion specifically for savings.

5. Lack of Financial Goals

Without clear financial goals, it’s easy to lose motivation and direction when it comes to saving money. If you’re not working toward specific milestones, such as building an emergency fund or saving for a home, your savings efforts might feel aimless. This lack of focus can lead to unnecessary spending and delayed progress. Set achievable goals with a timeline to give your savings purpose and structure. Breaking your goals into smaller steps can make them feel more attainable.

6. Ignoring Small Expenses

It’s not just big purchases that hurt your savings—small, everyday expenses can add up quickly. Things like daily coffee runs, subscriptions you forgot about, or frequent dining out may seem minor, but they can cost you hundreds each month. These “invisible” expenses are often overlooked because they don’t feel significant at the moment. Conduct a monthly audit of your spending to identify and eliminate unnecessary costs. Redirect that money into a savings account to see the difference it makes.

7. You Don’t Automate Savings

When you rely on leftover money at the end of the month to save, you’re less likely to stick to your savings goals. Without automation, it’s easy to spend what you intend to save, especially if you lack financial discipline. Automating your savings ensures that a portion of your income is set aside before you even have a chance to spend it. Treat your savings like a bill that must be paid each month. This “pay yourself first” approach builds consistency and grows your savings faster.

8. Overlooking an Emergency Fund

Without an emergency fund, unexpected expenses like medical bills or car repairs can derail your finances. Many people rely on credit cards or loans in emergencies, which can lead to debt and additional stress. An emergency fund acts as a financial safety net, protecting your long-term savings from being depleted. Aim to save at least three to six months’ worth of living expenses in a separate account. Having this fund gives you peace of mind and keeps your financial goals on track.

9. Lifestyle Inflation

As your income increases, it’s tempting to upgrade your lifestyle by spending more on non-essentials. This phenomenon, known as lifestyle inflation, prevents you from saving despite earning more money. For example, you might move to a more expensive apartment or buy a newer car instead of saving the extra income. While it’s okay to reward yourself occasionally, consistently spending more than necessary leaves little room for building wealth. Instead, increase your savings contributions whenever your income grows.

10. Neglecting Investments

Savings accounts are essential, but relying solely on them means you’re missing out on opportunities to grow your wealth. Inflation decreases the purchasing power of money over time, so savings that don’t earn interest lose value. Many people avoid investing because they think it’s complicated or risky, but not investing can cost you in the long run. Start small with low-risk options like index funds or retirement accounts to let your money grow over time. Investing helps you achieve financial goals faster while protecting against inflation.

11. Paying Too Much in Fees

Bank fees, credit card charges, and subscription renewals are easy to overlook but can significantly impact your finances. Overdraft fees, ATM charges, and account maintenance fees add up and eat into your savings potential. Similarly, unused subscriptions or services you rarely use are silent money-drainers. Regularly review your financial accounts to identify and eliminate unnecessary fees. Switching to no-fee banking options or negotiating lower rates on services can save you money in the long run.

12. Lack of Financial Education

If you don’t understand basic financial principles, it’s harder to make informed decisions about saving and spending. Many people struggle with managing money simply because they were never taught how. This lack of knowledge can lead to poor financial habits, missed opportunities, and unnecessary debt. Take the time to educate yourself on budgeting, investing, and personal finance strategies. There are plenty of free resources, from books to online courses, that can empower you to take control of your finances.

Struggling to save money often stems from hidden habits and behaviors that can be corrected with awareness and effort. By addressing these common issues—like overspending, neglecting goals, or overlooking small expenses—you can take control of your finances and build a stronger financial future. Saving money isn’t about sacrifice; it’s about making smarter choices that align with your goals. Start with one change at a time, and watch your savings grow steadily over time. Financial freedom is within your reach!