Maintaining financial stability is crucial for long-term security, but even seemingly minor mistakes can have significant consequences. Many people unintentionally undermine their finances with small errors that add up over time, leaving them struggling to make ends meet or achieve their financial goals. Recognizing these pitfalls and addressing them early can help you stay on track and build a secure future. Here are some simple errors that can derail your financial stability.

1. Ignoring a Budget

Failing to create and stick to a budget is one of the most common financial mistakes. Without a clear understanding of your income and expenses, it’s easy to overspend on non-essentials and neglect savings. A budget acts as a financial roadmap, helping you prioritize necessities, savings, and discretionary spending.

According to Investopedia, setting realistic spending limits and tracking expenses ensures that you live within your means. A well-planned budget is a foundation for financial stability.

2. Overusing Credit Cards

Relying too heavily on credit cards for everyday purchases can quickly lead to debt accumulation. High interest rates on unpaid balances make it difficult to pay off what you owe, leaving you in a cycle of debt. Paying off your full balance each month and avoiding unnecessary charges can save you significant money.

According to NerdWallet, limiting credit card use to emergencies or planned expenses is a smart way to maintain financial health.

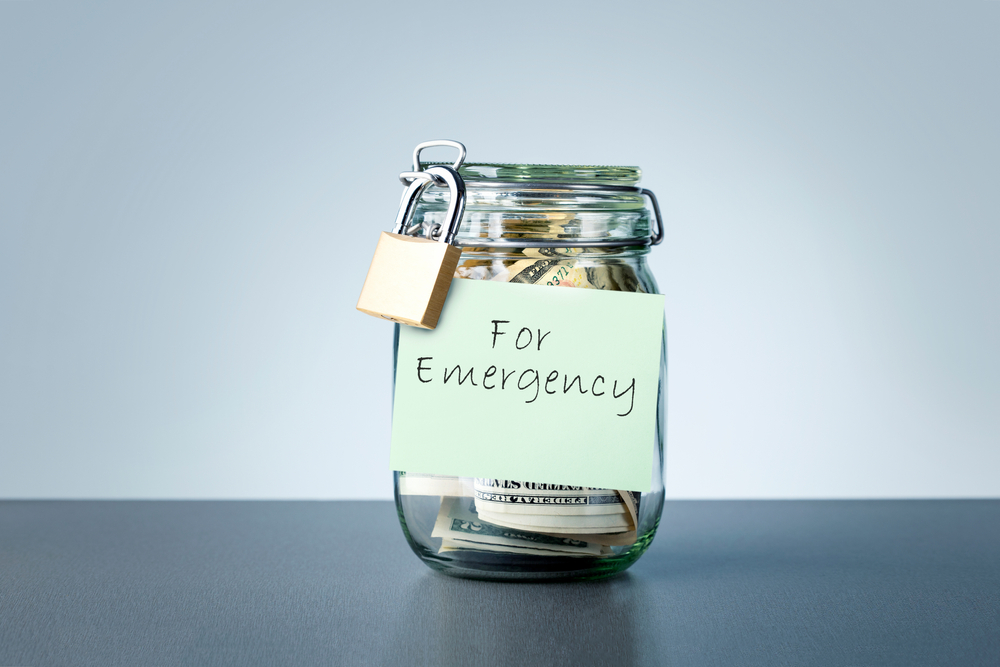

3. Not Having an Emergency Fund

An emergency fund is a critical safety net for unexpected expenses, like medical bills or car repairs. Without one, even small financial surprises can throw your budget into disarray and force you to rely on loans or credit cards. Saving three to six months’ worth of living expenses can protect you from financial instability.

According to Forbes, starting small and building your emergency fund gradually provides peace of mind.

3. Neglecting Retirement Savings

Postponing retirement contributions might seem harmless in the short term, but it can significantly impact your future financial security. By delaying savings, you miss out on the benefits of compound interest, which grows your investments over time.

Starting early—even with small amounts—can lead to substantial retirement funds. Take advantage of employer-sponsored plans or IRAs to ensure you’re preparing for the future, as noted by The Balance.

5. Overlooking Small Expenses

Seemingly minor purchases, such as daily coffee runs or frequent takeout, can silently drain your finances. These small costs, often referred to as “lifestyle creep,” add up over time and reduce your ability to save or invest.

Regularly reviewing your spending habits can help identify unnecessary expenses that eat into your budget. Cutting back on these extras and redirecting funds toward savings can significantly improve your financial health.

6. Skipping Regular Financial Check-Ins

Failing to review your financial situation regularly can lead to missed opportunities or overlooked problems. Without monitoring your accounts, you may forget due dates for bills, accumulate late fees, or neglect areas where you could save.

Scheduling regular check-ins to assess your income, expenses, and savings goals keeps you informed and proactive. Staying on top of your finances helps prevent avoidable setbacks and keeps you aligned with your goals.

7. Avoiding Insurance Coverage

Skipping or skimping on essential insurance, like health, home, or car insurance, can leave you vulnerable to significant financial losses. Unexpected emergencies or accidents can lead to high out-of-pocket costs that derail your financial stability.

Investing in adequate coverage protects you from unforeseen risks and provides peace of mind. Researching policies and comparing options ensures you’re adequately covered without overpaying.

8. Failing to Plan for Irregular Expenses

Large, irregular expenses—such as holiday gifts, annual insurance premiums, or vacation costs—can strain your finances if not planned for. Without setting aside funds for these predictable expenses, you risk overspending or going into debt. Creating a sinking fund, where you save small amounts regularly for upcoming big expenses, is an effective solution. Planning for irregular costs prevents financial stress and keeps your budget on track.

9. Not Negotiating Bills

Many people overlook the opportunity to negotiate bills for services like cable, internet, or insurance. Companies often have promotions or discounts available, but you won’t benefit unless you ask. Regularly reviewing your bills and negotiating for better rates can save you hundreds of dollars annually.

Being proactive about your expenses ensures you’re not overpaying for services.

10. Ignoring Investment Opportunities

Leaving your money in a low-interest savings account instead of investing it can limit its growth potential. Investing allows your money to grow over time, helping you build wealth and reach financial goals faster. While it’s important to understand the risks, ignoring investment opportunities can leave your money stagnant.

Researching beginner-friendly options like index funds or consulting with a financial advisor can help you get started.

11. Falling for Lifestyle Inflation

As your income increases, it’s tempting to upgrade your lifestyle with higher spending on cars, homes, or luxury items. This phenomenon, known as lifestyle inflation, often prevents people from saving or investing their additional earnings.

Practicing restraint and living below your means ensures you have extra funds for long-term goals. Directing raises or bonuses into savings or investments can help secure your financial future.

12. Failing to Pay Attention to Fees

Bank fees, credit card interest, and hidden charges in investment accounts can slowly chip away at your finances. Many people overlook these fees, but over time, they can add up to substantial amounts.

Regularly reviewing account statements and opting for low-fee alternatives can help reduce these unnecessary costs. Paying attention to the fine print ensures your money stays where it belongs—working for you.

Avoiding these common errors is key to maintaining financial stability. By being proactive, informed, and disciplined in your approach to money management, you can safeguard your finances and build a secure future. Small adjustments today can prevent big challenges tomorrow.