Saving money doesn’t have to be complicated or stressful. With the right strategies, anyone can build good financial habits that make saving effortless. Whether you’re trying to grow your emergency fund, save for a big purchase, or secure your financial future, small changes can lead to significant results. By adopting simple and effective money-saving techniques, you can improve your financial health without feeling deprived. Here are 15 strategies that make saving money super easy for everyone.

1. Automate Your Savings

One of the easiest ways to save money is to set up automatic transfers from your checking account to your savings account. This ensures that a portion of your income is saved before you even have a chance to spend it. Many banks allow you to schedule these transfers on payday, making it feel like just another bill to pay. Over time, the habit of saving without thinking about it builds financial security effortlessly. Even if you start with a small amount, the consistency of automatic saving adds up significantly over time.

To make automation more effective, consider setting up multiple savings accounts for different goals, such as an emergency fund, travel, or future investments. Some apps, like Digit and Acorns, automatically save spare change from everyday purchases. Treating savings as a non-negotiable expense ensures that you build wealth over time. If you receive unexpected income, like a work bonus or tax refund, automatically saving a percentage keeps you on track. Making saving a habit rather than an occasional effort leads to long-term financial success. According to CBS News, automating your savings can lead to consistent growth through compound interest and helps maintain financial discipline.

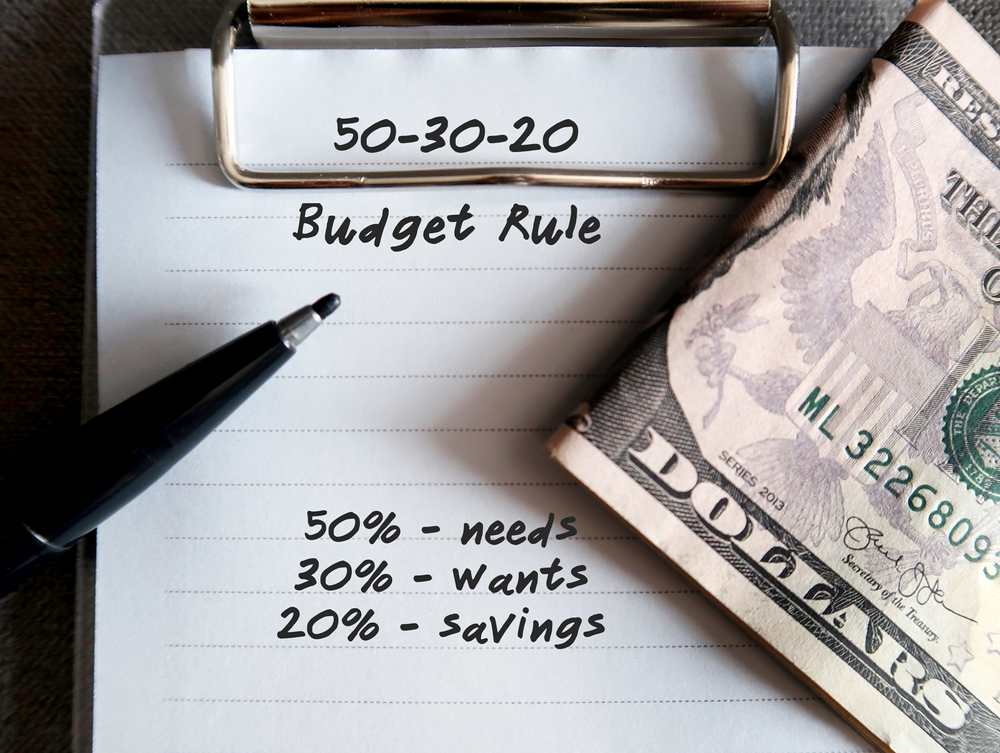

2. Use the 50/30/20 Budget Rule

The 50/30/20 rule is a simple yet effective budgeting method that helps you manage your finances while prioritizing savings. It suggests allocating 50% of your income to necessities such as rent, utilities, and groceries. Another 30% goes to discretionary spending, including entertainment, dining out, and hobbies. The final 20% is dedicated to savings and debt repayment, ensuring that you build financial stability over time.

This method provides structure without being overly restrictive, making it easy to follow. If 20% feels too high at first, you can start with a smaller percentage and increase it gradually. The goal is to create a balance between financial responsibility and enjoying life. Tracking your spending within these categories helps identify areas where you might be overspending. Using budgeting apps like Mint or YNAB makes it easier to stick to the 50/30/20 rule. Following this framework ensures that you meet financial goals while maintaining a comfortable lifestyle. As explained by Britannica, the 50/30/20 rule is a widely recognized strategy for balancing needs, wants, and savings.

3. Cut Out Unused Subscriptions

Many people waste money on subscriptions they no longer use or need. Streaming services, gym memberships, magazine subscriptions, and app fees can add up quickly over time. Reviewing your bank statements helps identify recurring charges that you may have forgotten about. Canceling subscriptions that no longer provide value frees up money for more important financial goals. Even eliminating just a few unused services can lead to significant savings each month. Apps like Rocket Money and Trim can track and cancel unused subscriptions on your behalf. Instead of signing up for multiple streaming platforms, consider rotating them based on what you’re currently watching.

If you rarely go to the gym, switching to home workouts or outdoor exercises can be a cost-effective alternative. Small adjustments in recurring expenses make a noticeable difference in your overall savings. Taking control of subscriptions prevents unnecessary spending and improves financial efficiency. According to MoneyHelper, regularly auditing your subscriptions can help identify and eliminate unnecessary expenses, saving you a substantial amount of money over time.

4. Cook at Home More Often

Eating out frequently can be one of the biggest drains on your budget. While dining out or ordering takeout is convenient, it often comes at a much higher price than home-cooked meals. Cooking at home allows you to control portion sizes, ingredients, and overall spending. Planning weekly meals helps you shop efficiently and avoid impulse purchases. Preparing meals in bulk also saves time and ensures you always have something ready to eat.

A great way to save even more is by learning simple, budget-friendly recipes. Using coupons and buying groceries in bulk further reduces food expenses. Packing homemade lunches for work instead of buying meals daily adds up to significant monthly savings. While it’s fine to enjoy an occasional restaurant visit, making home-cooked meals a habit keeps your finances in check. Developing good cooking habits leads to both financial and health benefits over time. As explained by Jamie Oliver, cooking at home can be both cost-effective and nutritious when done with smart planning and resourceful techniques.

5. Use Cash-Back and Rewards Programs

Cash-back programs allow you to earn money on purchases you were already planning to make. Many credit cards offer cash-back rewards for groceries, gas, and dining, making everyday expenses more rewarding. Some banks also provide debit card cash-back options, so you don’t need a credit card to benefit. Apps like Rakuten, Honey, and Ibotta provide additional cash-back savings when shopping online or in-store. Taking advantage of these programs can help you save hundreds of dollars per year.

To maximize rewards, it’s important to use cashback strategically rather than as an excuse to spend more. Always pay off credit card balances in full to avoid interest charges that negate any benefits. Combining store discounts with cash-back offers increases overall savings. Signing up for loyalty programs at frequently visited stores adds even more savings opportunities. Earning rewards on everyday purchases helps stretch your budget further without extra effort.

6. Set Clear Savings Goals

Having specific financial goals makes saving money more intentional and motivating. Rather than just saving aimlessly, defining what you’re saving for gives you a clear direction. Goals could include an emergency fund, a vacation, a down payment on a home, or early retirement. Breaking down large goals into smaller milestones makes them feel more achievable. Writing down your goals and setting a timeline increases the likelihood of staying committed.

Tracking progress toward your savings goals helps maintain motivation. Using goal-specific savings accounts ensures that money is allocated properly. Many banking apps allow you to set visual progress trackers to keep you focused. When you know exactly why you’re saving, it’s easier to resist unnecessary spending. Setting and reviewing financial goals regularly leads to consistent and successful saving habits.

7. Avoid Impulse Purchases

Impulse buying is one of the biggest obstacles to saving money. Many people purchase things on a whim, whether online or in-store, only to regret it later. To prevent unnecessary spending, implement the 24-hour rule—wait a full day before making any non-essential purchase. Often, you’ll find that the urge to buy fades, helping you save money. Creating a shopping list before heading to the store also helps prevent impulse purchases.

Unsubscribing from promotional emails and avoiding retail websites when bored can reduce temptation. If an item isn’t on your planned budget, consider whether it’s truly necessary. Using cash instead of credit cards for non-essential spending also makes you more conscious of how much you’re spending. Small impulse purchases may seem harmless, but over time, they add up significantly. Being mindful of spending habits helps you keep more money in your savings account.

8. Use a Separate Savings Account

Keeping your savings in a different account from your daily spending money prevents unnecessary withdrawals. A high-yield savings account offers better interest rates, allowing your money to grow faster over time. When savings are easily accessible, it’s tempting to dip into them for non-essential expenses. Placing your savings in a separate account makes it feel less like spending money and more like an investment in your future.

To strengthen this habit, consider opening an account that doesn’t have a debit card or easy transfer options. Some banks even allow you to lock funds for a specific period to prevent premature spending. Separating short-term and long-term savings ensures that you don’t deplete your funds unnecessarily. Having a dedicated account for emergencies, vacations, or major purchases gives financial clarity. Keeping savings out of sight makes it easier to resist unnecessary withdrawals.

9. Buy Generic Instead of Brand-Name Products

Many brand-name products are priced higher simply due to marketing and packaging, even when their ingredients or quality are nearly identical to generic versions. Supermarkets, pharmacies, and even clothing stores offer generic alternatives that provide the same value at a lower price. Household items like cleaning products, over-the-counter medications, and pantry staples often have generic options that save you money. Making the switch can lead to significant savings over time.

Before purchasing, compare labels to ensure that generic and brand-name versions have similar ingredients. Many retailers even offer satisfaction guarantees on their store-brand products, making the switch risk-free. While there may be certain items where the brand name offers noticeable benefits, most everyday essentials don’t require paying extra. Being open to generic options prevents overspending without compromising on quality. Choosing wisely between brand-name and generic products stretches your budget further.

10. Take Advantage of Discounts and Coupons

Using discounts, promo codes, and coupons can lead to significant savings on everyday purchases. Many grocery stores and online retailers offer loyalty programs that provide exclusive deals. Websites like RetailMeNot, Honey, and Coupons.com help you find discounts before making a purchase. Stacking coupons with existing sales can maximize savings, reducing costs on necessities.

Signing up for store reward programs or cashback apps helps you save on frequent purchases. Many credit cards also offer special discounts with partnered stores, making it easier to reduce expenses. Planning purchases around seasonal sales and clearance events further increase savings. Taking a few extra minutes to search for deals before checking out can result in long-term financial benefits. Incorporating discounts into your shopping habits makes saving money a routine rather than an occasional effort.

11. Pay Off Debt Faster

Carrying high-interest debt makes saving money much harder. Credit card interest, personal loans, and other debts accumulate over time, eating into potential savings. The longer you take to pay off debt, the more you lose in interest payments. By prioritizing debt repayment, you free up more money for future financial goals. The debt snowball method (paying off the smallest debts first) or the avalanche method (focusing on high-interest debts) helps speed up repayment.

Reducing monthly expenses and putting extra funds toward debt eliminates financial burdens faster. Refinancing or consolidating loans can also lower interest rates, making payments more manageable. The key is to avoid accumulating new debt while paying off existing balances. Once debts are cleared, the amount previously used for payments can be redirected into savings. Becoming debt-free increases financial security and makes long-term savings goals more achievable.

12. Embrace Minimalism

Minimalism isn’t about depriving yourself but focusing on what truly adds value to your life. Many people accumulate unnecessary items that don’t contribute to happiness or financial security. Reducing clutter and avoiding unnecessary purchases helps you save money while simplifying your lifestyle. Instead of spending on impulse buys, investing in quality over quantity leads to better long-term satisfaction.

Before making a purchase, ask yourself if it serves a real purpose or is just a temporary desire. Cutting back on excessive shopping, unnecessary gadgets, and fast fashion prevents wasted spending. Selling or donating unused items not only declutters your space but also reinforces mindful spending habits. Financial freedom comes from spending on things that truly matter rather than accumulating material possessions. Adopting a minimalist approach makes saving money effortless.

13. DIY When Possible

Hiring professionals for simple tasks can be expensive, but many repairs and projects can be done yourself with minimal effort. Learning basic home maintenance, car care, and cooking new meals reduces costs significantly. DIY solutions allow you to develop valuable skills while saving money on services. Online tutorials, YouTube videos, and instructional guides make it easier than ever to take on small projects independently.

Instead of immediately replacing broken items, consider whether they can be repaired first. Small household fixes, like unclogging a drain or repainting furniture, are manageable with the right tools. Even DIY gifts and home décor can save money compared to store-bought alternatives. Being resourceful with everyday tasks helps cut costs without sacrificing quality. Developing a do-it-yourself mindset ensures long-term financial savings.

14. Sell Unused Items

Decluttering your home and selling unwanted items can provide extra cash while freeing up space. Many people hold onto things they no longer use, unaware of their resale value. Platforms like Facebook Marketplace, eBay, and Poshmark make it easy to sell electronics, clothing, and furniture. Even small sales add up over time, providing funds that can go directly into savings.

Regularly reassessing your belongings prevents unnecessary accumulation. Instead of letting valuable items collect dust, turning them into cash benefits both your finances and your living space. Hosting garage sales or selling locally through apps can generate quick income. Setting a goal to sell a few items each month builds a habit of financial resourcefulness. Making money from unused items turns clutter into a financial opportunity.

15. Plan Purchases Around Sales

Timing your purchases around major sales events helps reduce costs on big-ticket items. Black Friday, Cyber Monday, end-of-season sales, and holiday discounts offer significant savings opportunities. Researching prices in advance prevents overspending on full-price items. Many retailers also provide price matching, ensuring you get the best possible deal.

For major expenses like electronics, appliances, and furniture, waiting for the right sale makes a noticeable difference. Subscription services, travel bookings, and clothing also have peak discount periods. Being patient and strategic with spending allows you to maximize savings effortlessly. Instead of buying impulsively, planning ensures your budget stretches further. Taking advantage of discounts turns necessary spending into smart financial decisions.

Saving money doesn’t have to be difficult—it’s about making small, intentional choices that add up over time. Automating savings, cutting unnecessary expenses, and using smart budgeting techniques help you reach financial goals with minimal effort. By implementing these strategies, you can take control of your finances and build a strong foundation for long-term financial success. The key is consistency—start with a few changes and gradually incorporate more for effortless saving.